The global financial architecture is once again under scrutiny as calls for reform grow louder. For Africa, this conversation has never been more urgent. The continent faces a host of economic challenges—debt sustainability, limited access to credit, high borrowing costs, and inadequate financial infrastructure—issues that global economic disruptions have exacerbated.

As Africa pushes for greater inclusion in global financial reforms, most notably with the African Union’s recent membership in the G20 (now G21), it is clear that building a resilient financial system within the continent must be a parallel priority.

Africa’s relationship with the global financial system is characterized by significant imbalances. African economies often grapple with high borrowing costs, restricted access to international capital markets, and stringent conditions imposed by international financial institutions. For instance, Zambia and Ghana have faced severe debt crises resulting from unsustainable borrowing practices, compounded by volatile global markets and interest rate hikes by major central banks.

Similarly, Ghana suspended payments on most of its $30 billion external debt in December 2022, citing the economic fallout from the COVID-19 pandemic. In May 2024, Ghana reached a memorandum of understanding with bilateral creditors, including China and France, to restructure $5.4 billion of its debt. This agreement enabled the International Monetary Fund’s (IMF)’s approval to disburse $360 million under a $3 billion three-year bailout program. (Source)

These cases highlight the pressing challenges African nations face in debt management and underscore the urgent need for structural reforms to ensure long-term economic viability.

Additionally, Africa’s share of global credit flows remains disproportionately low. Despite the continent’s immense growth potential, international investors remain risk-averse, driving up borrowing costs and limiting access to vital funding for infrastructure, healthcare, and development projects. This has left many African economies over-reliant on external aid and debt.

While global reforms to create a fairer, more inclusive financial system are essential, Africa must also look inward to strengthen its financial architecture. Building a resilient African financial system should be the foundation upon which any global reforms can stand. This entails several key actions: African countries need robust frameworks to manage and restructure existing debt.

The African Union (AU), the African Development Bank (AfDB), and other regional bodies must play a more active role in debt negotiations, pushing for multilateral mechanisms that prioritize African interests. Transparent debt management strategies can prevent future crises and build investor confidence.

To simultaneously address the debt crisis and climate challenges, debt-for-climate swaps offer an innovative opportunity for Africa. These mechanisms allow countries to restructure their debt in exchange for specific commitments to climate action, such as ecosystem restoration or investments in renewable energy. Several African leaders, including Kenya’s President William Ruto, have championed these approaches which appear to be gaining traction in international forums.

High borrowing costs often stem from perceptions of risk. By developing a more resilient and integrated financial system, African countries can work towards more favourable credit ratings, thereby reducing the cost of capital.

Establishing a pan-African financial infrastructure, leveraging digital finance, and promoting regulatory harmonization could create an enabling environment for intra-African trade and investment, boosting growth from within.

The African Union’s (AU) recent inclusion in the G20, marks a significant milestone. As Africa’s official representative in one of the world’s most influential economic forums, the AU now has an unprecedented opportunity to influence global financial reforms.

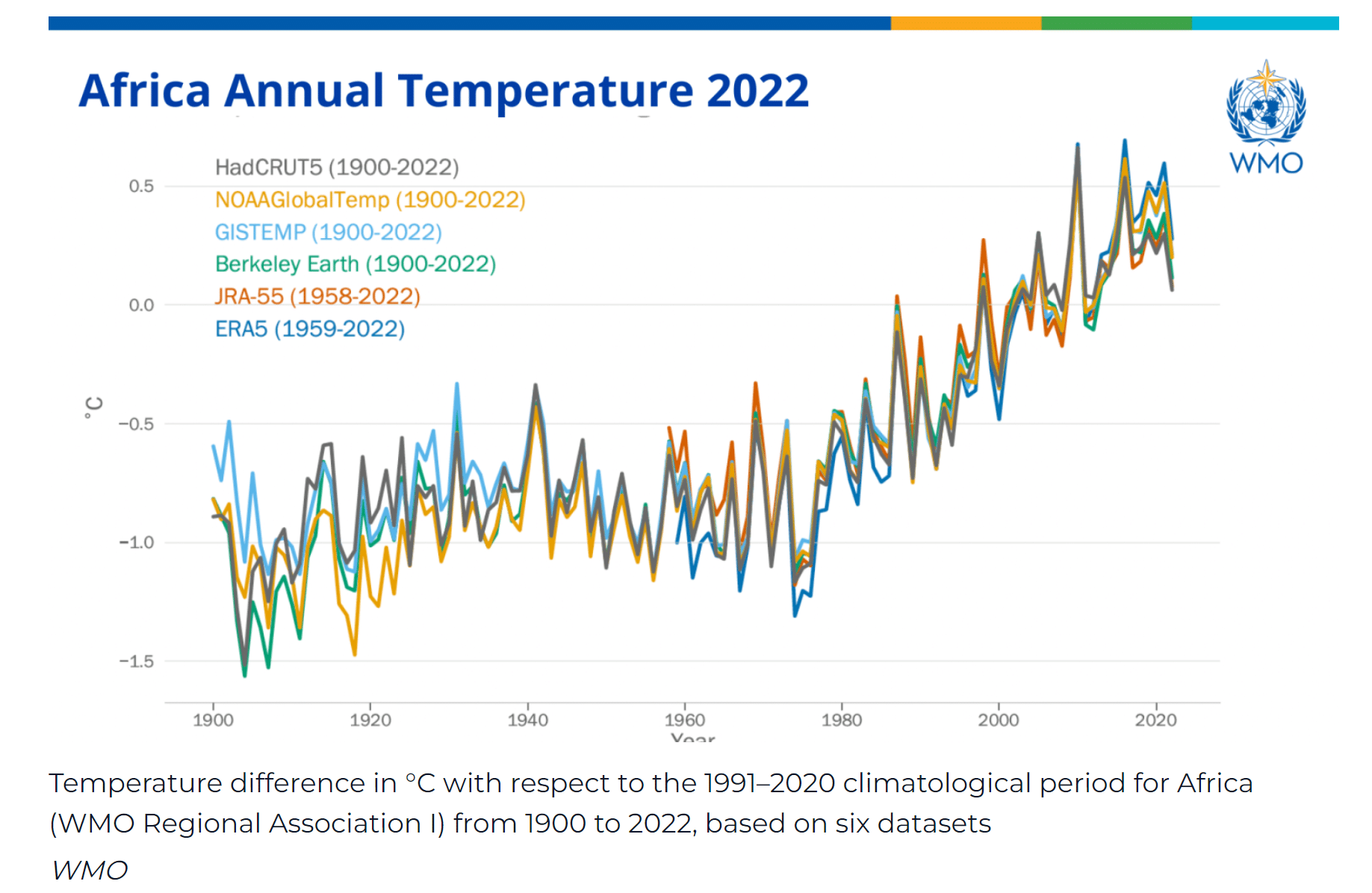

The G20 represents around 85% of global GDP and 75% of global trade. This is particularly crucial as Africa faces some of the world’s most pressing challenges, such as the climate crisis, which disproportionately affects the continent despite its minimal contribution to global emissions. In 2022, over 110 million people in Africa were directly impacted by weather, climate, and water-related hazards, resulting in economic damages exceeding US$ 8.5 billion.

Despite contributing less than 10% of global greenhouse gas emissions, Africa is the continent least equipped to handle the adverse effects of climate change.

The African Union’s key priorities in the G20 should include advocating for global frameworks that provide equitable debt relief and restructuring mechanisms, particularly for African nations disproportionately affected by global economic shocks. According to the UN Economic Commission for Africa, Africa requires approximately $1.3 trillion in annual investments to achieve the Sustainable Development Goals (SDGs) by 2030.

Additionally, the AU should aim to secure increased access to climate financing, leveraging its G20 membership to ensure Africa receives its fair share of the $100 billion per year pledged by developed nations for climate adaptation and mitigation.

Africa stands at a critical crossroads. While the continent engages in global financial reform discussions, it must also prioritize strengthening its economic foundations. Debt-for-climate swaps, equitable access to climate finance, and innovations such as digital financial services are not just tools but pillars of a broader strategy to build a resilient financial system. As Africa seeks a stronger voice in the global financial system, it must remember that true reform starts from within.