President Donald Trump in recent weeks has changed his tariff policies more often than some of us change our clothes. The velocity of tariff changes has probably provoked a few nervous breakdowns in the accounts department of American companies trading goods with Mexico and Canada. So far, the African continent has been largely unaffected. The question ahead of 2 April, Trump’s “liberation day”, when he unveils his tariff plans, will we still be so relaxed?

We think the continent can, mostly, relax.

What does the Trump administration want to achieve with his trade war?

Many are still unsure what the Trump administration’s goal is with tariffs.

Why does it matter? Because it means analysis of the potential tariffs on 2nd April are over-complicating the issue. There is too much focus on scenarios like “reciprocal tariffs” (the US will match the tariffs others use against the US), or “including VAT tariffs” (because of the potential US stance that value-added tax act as a de facto tariff).

For reasons we outline below – in this piece we consider just three scenarios.

- The US tariffs everybody

- The US tariffs everybody who runs a trade surplus with the US, and

- The US tariffs everything except commodities that the US imports.

One political consultancy last week told us that the US wants to use the threat of tariffs as leverage for others like the EU or India to cut their tariffs. In the end, tariff threats today may lower global tariffs and therefore boost global trade. We think this is the US Treasury secretary’s hope; however, it does not reflect the rhetoric of the President. We believe this outcome is highly optimistic.

Others focus on the US President’s fond reminisces about the 19th century when tariffs were responsible for most US government revenues, and his hope that tariffs will fund tax cuts. This position ignores the fact that US government spending was less than 10% of GDP in the 19th century, while today it is over 30% of GDP. Tariffs cannot possibly replace income taxes, but yes, at the margin it may help the deficit.

Another view is that the current administration genuinely believes it can create a manufacturing renaissance in the US, with American sweatshops of the 19th century rising again and displacing imports from Asia or Africa. We will be a little surprised if Americans want to compete with the $100-$200 monthly wages of Bangladesh. We also note that in President Trump’s first term, foreign direct investment in the US fell, so the policy did not work.

Our reading of the President’s biographies suggests his tariff views might be viewed as deeply personal. President Trump hates weakness and sees deficits as a weakness which might infect the US. As such, the focus is rarely on the service sector, where the US runs a surplus, but only about trade where it runs a deficit. The current policy stance might not recognise that buying cheap t-shirts from abroad allows Americans work in higher value-added jobs at Google and saves them money so they can spend more at home. As imports are a

small share of the US economy, the import bill is not greatly negative. We pencil in the assumption that the US imposes 10% tariffs but recognise this may be just against countries who have a trade surplus with the US.

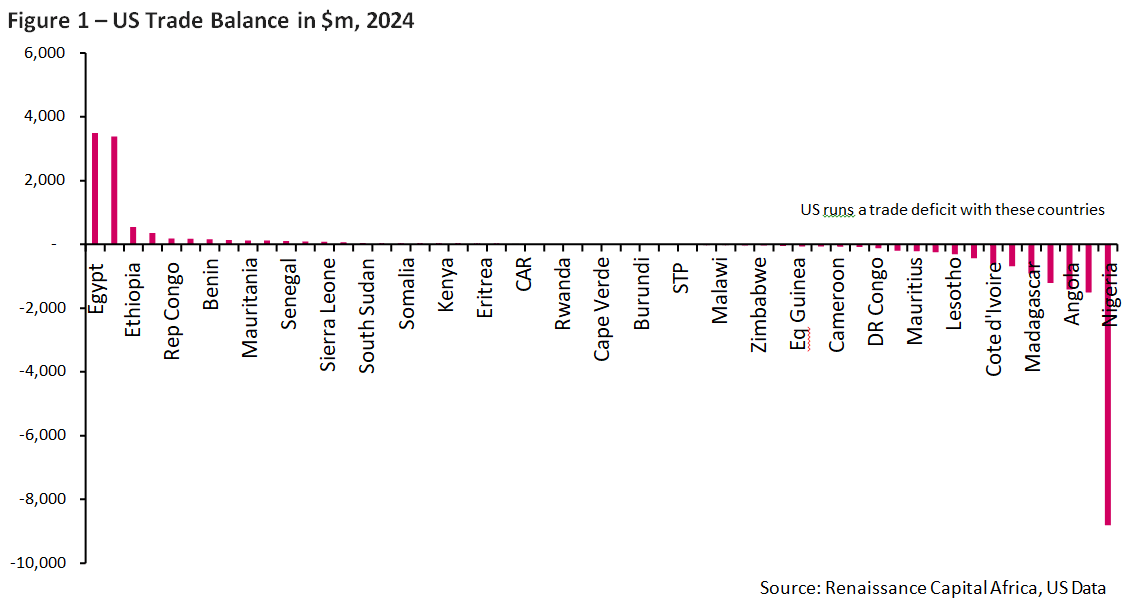

Who does the US have a trade deficit with?

If there is one African country that should be more worried than most, it is South Africa. They are not having it easy, given the cabal of South African immigrants whispering into the US President’s ear. It is perhaps bad timing for South Africa to have a $9bn trade surplus with the US. South Africa’s potential exclusion from AGOA and an inclusion of 10% tariffs both seem eminently plausible.

The next three countries in the proverbial firing line are Nigeria, Algeria and Angola.

Two of the Trump administration’s favourite African countries, Egypt and Morocco, run deficits with the US, thus if any countries on the continent are going to escape 2nd April unscathed, it should be these two. Indeed, over half the continent can argue the case that they run deficits with the US. It wouldn’t surprise us if they are untouched.

The commodity experts have noticed that the US is running the biggest trade deficits with Africa’s biggest commodity exporters. Over half of South Africa’s exports to the US are precious metals, diamonds, jewelry and platinum. The vast majority of Nigeria, Algeria and Angola’s exports are oil.

Is the US administration so focused on signaling strength as to tariff the commodities that US industry wants, or the US oil industry refines so it can sell back to Africa?

Yes.

The US has already begun an investigation into copper, which might see tariffs enacted on that mineral. This is why copper prices are surging in recent weeks, as stockpiles are built up, just in case. While there was talk of a lower 10% tariff being imposed on Canadian oil vs 25% on Canada’s other exports, in the end this did not happen.

Does it really matter to an oil exporter if the US imposes tariffs? Not much.

Exporters can divert their oil to any other country. The same will be true of most commodities.

How important is the US as an export destination for any African country?

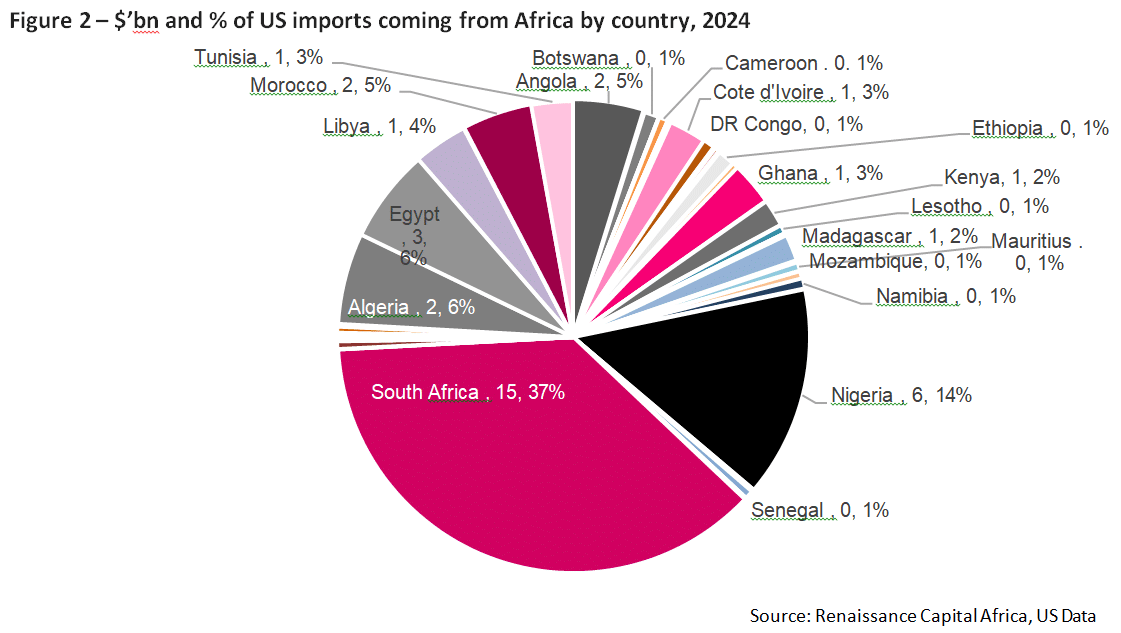

The US does not trade much with Africa. It imported $39bn of goods in 2024, which is roughly what it imports from Mexico or Canada in just over a month. The US imports more in 24 hours from either of them (over $1bn a day), than it imports in a year from about 40 African countries. The biggest exceptions are South Africa and to some extent Nigeria, which account for over half of everything the US imports from the continent.

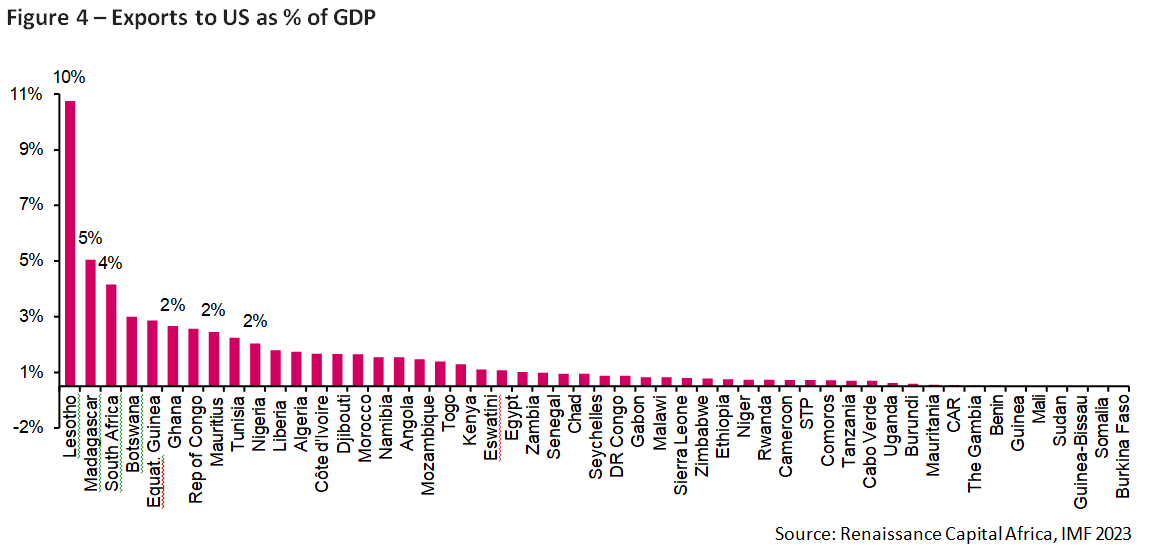

Fortunately for most African countries, the US is not that important either. For over half the countries in Africa, the US accounts for 2% or less of total exports.

Share of exports is however not the right metric. Instead, we need to understand how open an economy is, by examining how high exports are as a proportion of GDP. So, the best metric is to look at “exports to the US” as a share of the exporting country’s GDP.

When we do this, we find it is Lesotho which gets hit hardest. Its exports to the US are equivalent to 10% of its GDP. That’s particularly unfair because Trump doesn’t believe anyone has even heard of Lesotho.

How much pain would be imposed by 10% US tariffs. We should assume that US retailers may cut their margins by a 2-3%, and Lesotho exporters may do the same. Together that could halve the impact of the tariffs. We might see some currency weakness against the US dollar – even just 5% would then offset the remaining impact.

We can be more bearish and suggest 10% tariffs cut exports to the US by 5% and being extra bearish, assume that countries cannot re-direct their exports elsewhere. For Lesotho, that would cut GDP by about 0.5%, but it is an extreme and unlikely scenario. For South Africa, that would be an impact worth 0.2% of GDP (5% of the 4% of GDP figure above). For Nigeria, the impact would be half this at 0.1% of GDP. But this is surely an exaggeration, because Nigerian oil can be sold elsewhere.

What about indirect effects of Trump’s trade wars?

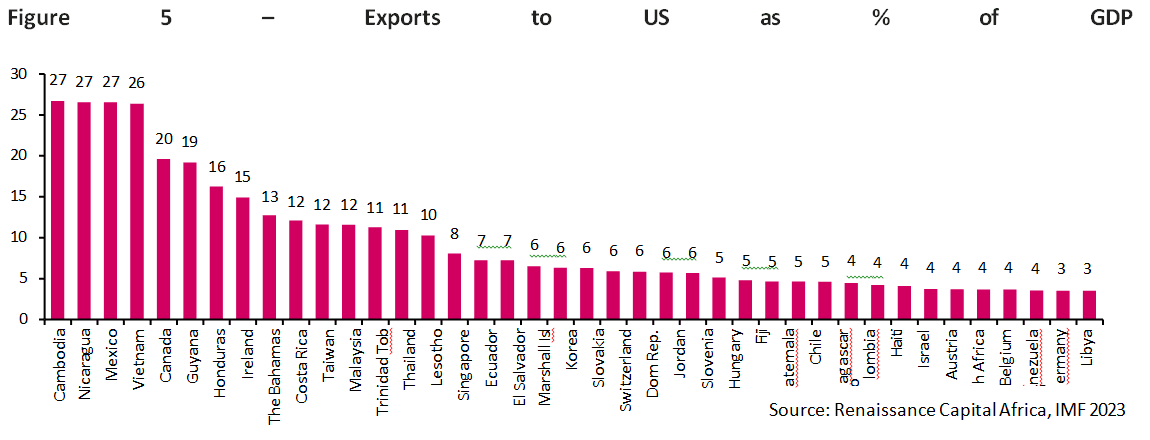

Should anyone worry about the Trump administration’s tariffs? Yes. There are 14 countries (excluding a few tiny islands) where exports to the US as a share of GDP are higher than Lesotho. Mexico and Vietnam have 27% of their GDP coming from exports to the US. A worst-case 5% hit to that figure from 10% tariffs would strip 1.35% off economic output.

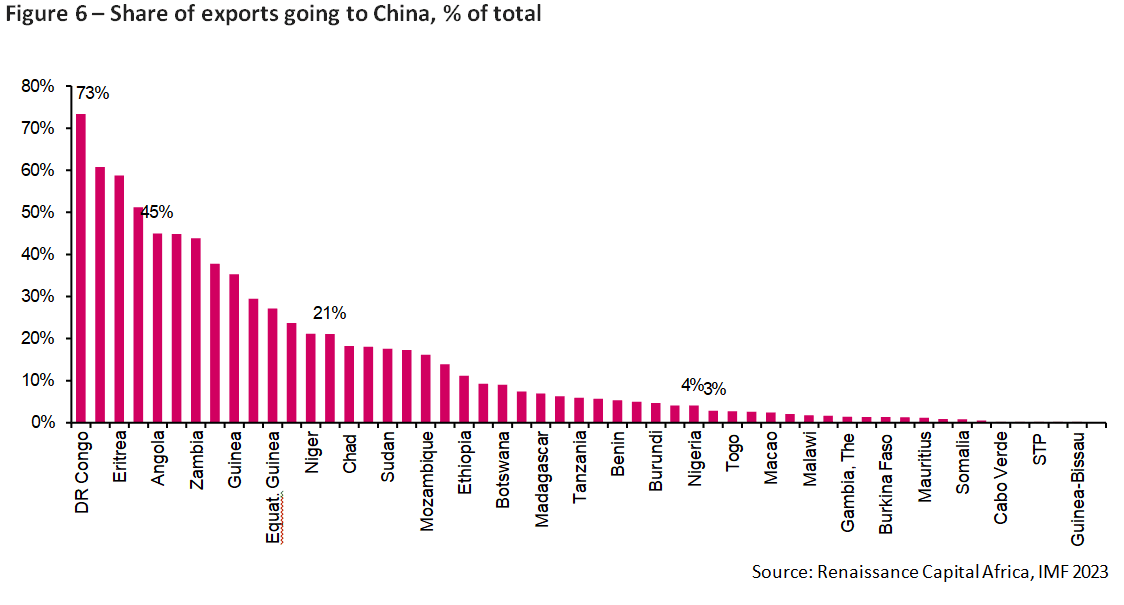

This would be more painful if tariffs are higher than 10%. For the EU and China, we think there will be (tariffs on China have already been hiked to 20% since Trump took office in January). Germany, still one of the world’s top 5 economies could suffer more if the tariffs imposed on the EU are around 25%. If exports drop 10-15%, that might be a 0.4% of GDP hit. We know Germany is planning on a fiscal bazooka to lift its economy and balance the effect of tariffs. GDP growth is likely to accelerate versus the pre-Trump baseline, even if he imposes 25% tariffs; so, Germany may buy more from the rest of the world, including Africa. What about China, where the Trump administration has talked about 50-60% tariffs? Only 2% of China’s GDP comes from exports to the US, so an absolute worst-case scenario would not see more than 0.5% of GDP taken off China’s growth, and China is promising fiscal stimulus too. Any slowdown in China would matter more to Africa. The share of South African exports going to China is double that going to the US. It does not look likely that US tariffs will cause a very high amount of pain to China, or to its trading partners.

Nonetheless, some small indirect impact on Africa is likely to come from Trump’s tariffs. Global trade is likely to be hit, cutting demand for energy, and pushing oil prices down. Even here, we should be cautious. Global trade may just be re-directed as happened in 2018 when China stopped buying soyabeans from the US and bought them from Brazil instead regardless of the longer shipping route. Consequently, US soyabean exports took Brazil’s previous export markets, again probably adding to shipping and fuel costs.

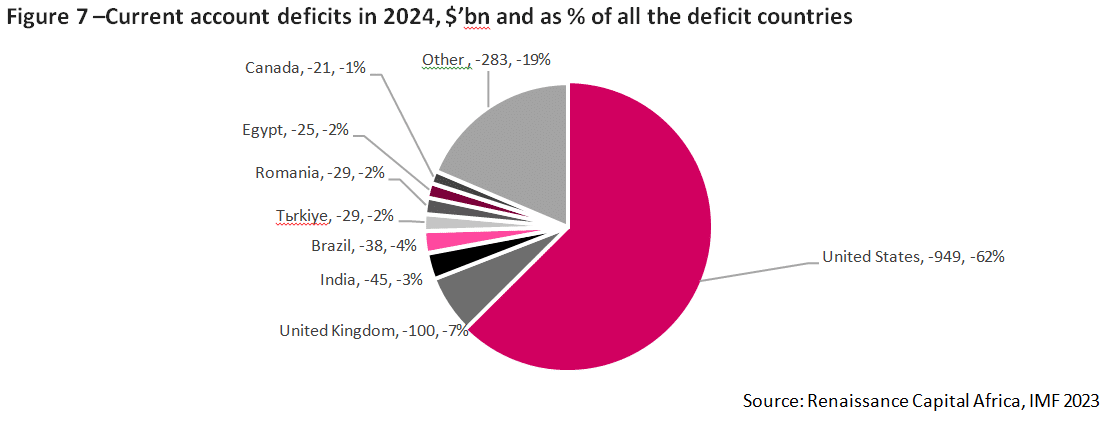

The key point is that the US is not the only economy in town. Yes, it is responsible for half the world’s current account deficit, so it matters, but it doesn’t matter too much to Africa.

What about inflation and US interest rates?

Should Africa worry because tariffs are inflationary and they might prompt the Fed to raise interest rates, or cut interest rates less than expected?

The last thing we want to see on the continent is more countries running onto the default rocks. From Mozambique to Senegal, we can see that is still a risk. The Fed kind of answered this question last week. They see tariffs as transitory (yes, we have heard that before), because while there will be a one-off adjustment in prices, there should not be a price-wage spiral as we saw after COVID.

That might underestimate where the Trump administration goes with tariffs. Their last trade war did not achieve preset objectives. The deficit with China remained massive. Perhaps this time the target is to succeed via a continuous ramping up of tariffs. We cannot know this, but at least today, we can be comforted by the Fed’s view that tariffs are a negative for GDP growth, and more important than the inflation impact. As such, the FED assumes two fund rate cuts in this year and another two next year.

Conclusion

We cannot be sure if the Trump administration will impose tariffs on any African countries at all, and if he does, he might go after only the minority of countries. We do not believe AGOA will offer any more protection than NAFTA did in 2016, or its successor USMCA has done in 2025. We do think South Africa is likely to face tariffs, and that it will be Lesotho which gets hit hardest if Trump imposes universal tariffs.

Our most important conclusion is that Trump’s tariffs won’t matter too much, assuming they’re just 10% on Africa.

Enjoy April and be thankful you did not emigrate (japa) to tariff-hit Canada.